Ask a Money Therapist: Feeling guilty spending money, debt anxiety, and rigidity

What You Need to Know About Money & Emotions:

Money is emotional: Transitioning from saving to spending can feel emotionally unsafe, even when the math says you’re ready.

Defining shared expenses: Going over shared expenses in a relationship isn’t a failure; it’s a sign your system may need adjusting.

Anxiety and debt often go hand-in-hand, and you don’t have to fix everything at once to feel better.

Ask A Money Therapist

As a financial therapist (Google tells me some people call me a “money therapist”), I don’t just talk about budgeting or debt payoff strategies (though those may come up). I work at the intersection of money and mental health—helping people understand the why behind their financial patterns, explore the emotions that come with money decisions, and develop systems that feel aligned and sustainable.

In other words: I help people make sense of their money feelings and move forward without shame.

Below are three real questions from my community—each one touching on a different financial season. If you’ve ever felt scared to spend, confused about shared expenses, or overwhelmed by debt anxiety, there’s something here for you, too.

“How do I transition from saving to spending in retirement?”

“So much financial education is focused on saving and it is so difficult to spend now. I'm approaching retirement, but I still find myself saving around 35% of my income and maxing out my TSP and Roth IRA, always looking for and waiting for different deals.

My investments continue to grow, and I have more than enough, but I can't seem to break this super saver mentality. I know I'm fortunate. I have a job with a pension and healthcare with a minimum retirement age of 57. Why am I scared to spend money on myself? I keep telling myself that I'm saving so much money so I can take early retirement with no concerns.

I recently bought my dream luggage, and I'm planning three trips next year. You might remember me from the Not Another Budgeting Challenge!”

First off—YES to the dream luggage and travel plans! And thank you for joining that challenge. (psst, if you want to join the Not Another Budgeting Challenge, get on my email list hereand I’ll send you all the details!) What you’ve described here is something I see often in my practice: you’ve worked hard, saved diligently, and done all the “right” things... but spending still feels scary.

This is where money therapy comes in. Because even when the numbers say “you’re good,” your nervous system might still say, “it’s not safe.”

Here are some tips I’ll extend for someone working on moving from saving to spending in retirement:

Mindset shift. A simple mindset shift I offer clients is this: “I worked hard to save money to keep my future self safe, and now I can practice safety by enjoying what money affords me.” That little “and” is the invitation. It helps bridge your past self’s goals with your present self’s desires.

Give your money a job, a spending job. If you’re still feeling that internal tug-of-war, try creating a fun money account, something I recommend all the time. Labeling a specific account as “fun money” can help your brain understand that the money in this bucket is meant to be spent. It gives you a cue that it’s safe to enjoy it. You might set up:

A general savings account

A travel fund

A fun money account for everyday joy

In short, what’s the point of working so hard to save your money if you can’t let yourself enjoy it?

“How to split expenses as a couple? We keep going over our shared expenses. Should we just cut back?”

“My partner and I live together and share an account for shared expenses, things like rent, groceries, and utilities. But we keep separate accounts for individual expenses such as our self-care spending and hobbies.

The problem is that we keep going over our shared expenses budget and pull from our individual accounts to cover things like movies or concerts.

At the end of the month, should we be contributing more to our shared expense account or just cut back generally on entertainment altogether so we stop dipping into our individual accounts?”

Trying to figure out how to split expenses as a couple is one of the most common themes that I hear from couples.

The good news is that you’ve got a system in place: shared account for joint needs, personal accounts for individual stuff. In practice, it’s not quite holding up. That gives you some good information that the system needs to be tweaked. Here are some ideas to help you modify your financial system.

Don’t restrict (yet). Before you slash the entertainment budget, zoom out. Ask yourselves:

Is the category (entertainment) the problem?

Or is the amount you’re contributing to shared expenses just too low?

If the only issue is that your joint account is running low while your personal accounts are still stable, that’s a sign to consider increasing your shared contributions, not necessarily cutting back.

Use the data: Look back over a few months and tally up what you’ve actually spent on shared fun—concerts, takeout, date nights. Then compare that to what you’ve been budgeting. If your other financial goals (saving, bills, etc.) are still being met, then giving more money to shared joy is an aligned shift. However, if you’re burning through both shared and personal accounts, then that’s your cue to reevaluate and reprioritize.

And a little legal reminder: If you’re living together and sharing significant expenses but aren’t legally partnered, I encourage you to have a conversation about financial protections. Whether it’s a lease, a house, or just a utilities account, some clarity on what happens if things change is an act of love. I’ve got a whole post all about how to protect yourself legally and financially if you aren’t married.

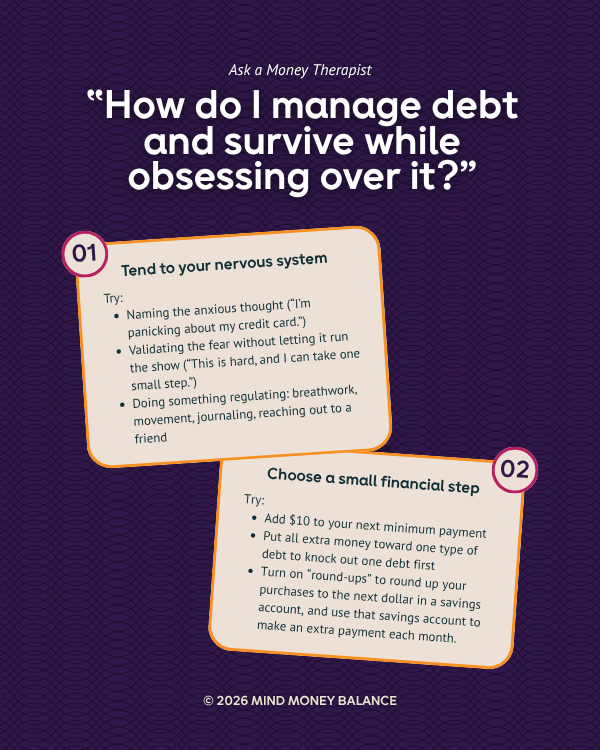

“How do I manage debt and survive while obsessing over it?”

“How do I manage debt and survive while trying to work through financial anxiety and obsessing over it?”

First: deep breath. Money is emotional, and so many people (most people!) experience this emotional distress around their finances.

Anxiety and debt are both heavy on their own. When anxiety and debt are combined, they can create a feedback loop that’s hard to break:

I’m anxious → I avoid or obsess → I feel worse → repeat.

There are two things you can do. Normally, I tell people to focus on one thing at a time, but in this case, I’d invite you to think about these tips running in parallel so you can get where you need to go.

Track One: Tend to your nervous system. When your brain is in “fix everything now” mode, even a small financial task can feel enormous. So your first step is emotional grounding. Try:

Naming the anxious thought (“I’m panicking about my credit card.”)

Validating the fear without letting it run the show (“This is hard, and I can take one small step.”)

Doing something regulating: breathwork, movement, journaling, reaching out to a friend

Track Two: Choose one small financial step. Try doing one small thing to pay down your debt a little faster. Here are a few ideas:

Add $10 to your next minimum payment

Put all extra money toward one type of debt to knock out one debt first

Turn on “round-ups” to round up your purchases to the next dollar in a savings account, and use that savings account to make an extra payment each month.

There’s a myth in personal finance that you have to go “all in” or do nothing. That’s just not true, especially when anxiety is involved. And yes, you’re allowed to enjoy life even while you’re paying down debt.

Money therapy meets you where you are

Whether you’re trying to shift from saving to spending (in retirement or otherwise), manage money with a partner, or cope with debt anxiety, the “right answer” isn’t a cut-and-paste answer.

It’s about checking in with what feels best for you in your life, and making small tweaks that help you feel better.

Financial therapy helps you name what’s actually going on and offers tools to help you move forward from a place of care. Stay informed about different ways you can get financial therapy tips, including ways to work with Lindsay, by joining the Mind Money Balance email newsletter.