100: Budget vs. Spending Plan For Couples

What is a Budget?

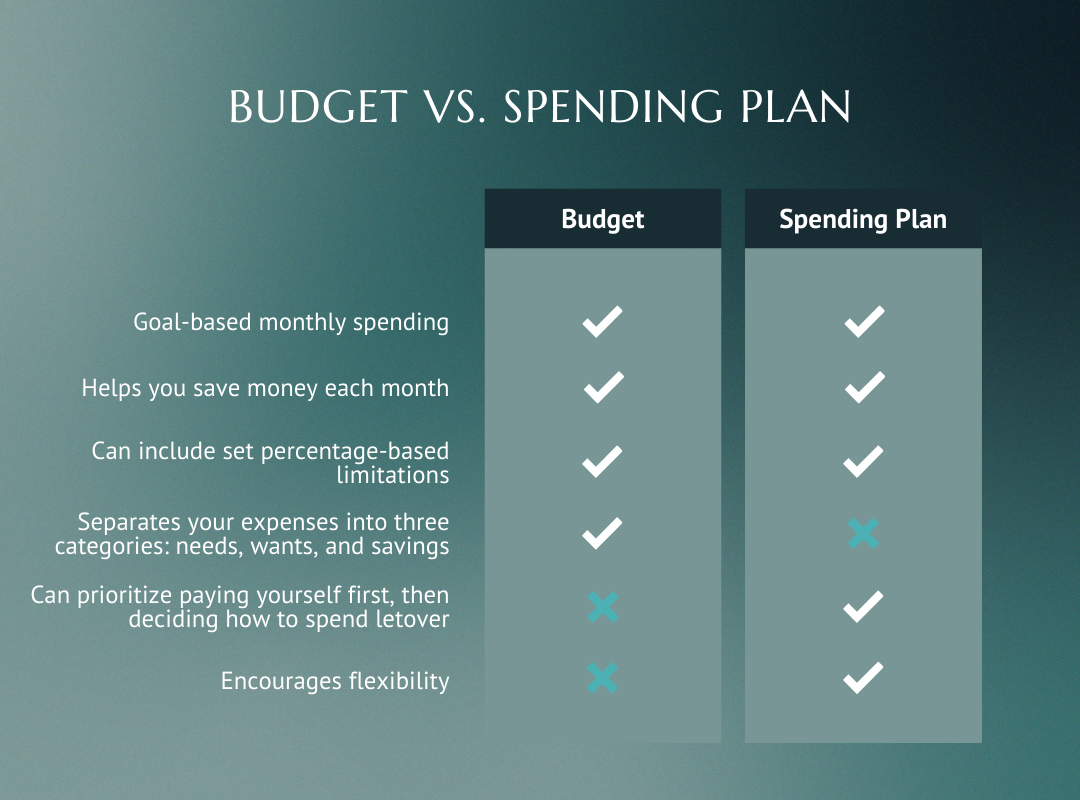

A budget is a financial planning tool where you determine how much money you will spend or save each month. The first steps of a budget are understanding how much money you earn and how much you spend. The goal of a household budget is to make sure that you spend less than you earn. Spending less than you earn helps you save money each month and can prevent you from living paycheck to paycheck.

Most budgets separate your expenses into three categories: needs, wants, and savings. Needs are things like food, shelter, medication, and transportation, and wants are things like dining out, traveling, and upgrading electronics before your current ones break. Savings could be for short-term goals like upgrading your car, creating an emergency fund, or going toward investing money in retirement.

Often budgets are percentage-based, as in "you can spend 30% of your income on housing," or "I'm budgeting 25% of my income toward food and dining out expenses." Budgeting gets a bad rap because of its restrictive nature. Budgeting also tends to come with additional emotional baggage. If a client of mine makes a mistake with budgeting, they tend to say, "I'm just bad at budgeting." In couples, this sounds like, "we've tried budgeting because it doesn't work for us." Budgeting can often require rigid tracking and adhering to someone else's financial guidelines.

For example, a rule in the personal finance industry states that you should spend no more than 30% of your income on housing. Did you know that this "rule" derives from a 1979 HUD bill that caps public housing rent at 30% of a renter's income? It has nothing to do with the actual cost of rent or mortgages today.

What is a Spending Plan?

A spending plan is the same idea as a budget, with a nicer ring. A spending plan functions similarly to a budget in that you set goals for how much money you can safely spend each month. For some people, they set similar percentage-based limitations, whereas for others pay themselves first, then allow themselves to spend their leftover money however they'd like.

A spending plan vs. a budget is a powerful reframe to help couples find a method of tracking their income and expenses and making sure they save for goals and pay for their future selves. Many of my clients prefer the term because it feels more proactive and empowering than the term "budget."

A spending plan, in my opinion, also gives you more flexibility. For example, instead of saying something like "massages are a want, not a need," like many strict budgeters will tell you, you get to decide that you can spend it if there is money available to spend. I heard a Ramsey-er say that allowing yourself to spend on "wants" "encourages overspending and not prioritizing future security." This hyperfocus on rigid rules is precisely why so many budgets don't work. As a therapist, I know that strict rules for most people are bound to backfire. Instead, what's kinder is allowing ourselves the ability to enjoy while we are saving for our future. It's not black-or-white or all-or-nothing; it's both-and.

Why A Spending Plan is Important

A spending plan is the foundation of creating a healthy financial plan. Having a spending plan means you know how much money is coming into your household each month and that you have a flexible plan for how much money is going out each month. A spending plan that works for couples helps them ensure that they aren't living paycheck to paycheck. It also builds room for future planning.

Instead of a budget that says "you can only spend $X on things that fall into this category," a spending plan says, "you are allowed to spend up to $X on things in this category. And if you spend more? No big deal. You'll have to spend a little less on a different area."

When it comes to spending, my partner and I first save for things, then we spend. For example, my spending plan means that my partner and I autosave each month for student loans (currently on pause), vacations, gifts, and irregular expenses. Our spending buckets fill up after our money goes into designated savings buckets. For us, that looks like funding a general spending bucket that we use to pay for our mortgage, groceries, home maintenance, pet care, and transportation costs.

After that? Whatever money is left over can be spent how we like. For example, recent spending plan purchases included a celebratory birthday brunch with friends, a date night streaming a movie and ordering takeout and a last-minute visit with family. We each get a little bit of fun money to spend however we want as individuals.

A spending plan is working if you spend less money than you earn each month, have a system to track spending that works for you, you feel good about where your money is going, and the spending plan helps you communicate with your partner about your financial plan.

Budget for Couples Living Together

For cohabitating couples, having a budget or spending plan isn't just important for managing a household; it's also about creating intimacy. Agreeing with your partner about your current and future financial goals is like saying, "we want to be together. We see a future for us. We're investing in this relationship." Creating a spending plan and talking about money is incredibly vulnerable! It's a great way to collaborate on something that might feel awkward and uncomfortable and find a plan that works for you.

There are a few ways couples can set up their spending plans or budgets.

Joint "Ours"

All money is pooled in a joint account, all expenses are paid from the joint account

Separate "Mine" and "Theirs"

Money earned and spent is separate.

Some couples decide to each pay certain bills, whereas others send Venmo or Zelle requests back and forth.

Hybrid "Theirs," "Mine," and "Ours"

There are three different accounts in this method: a joint account where some of each person's income goes and joint expenses come from that account, and two separate accounts for each person.

A 2021 paper by the University of London found that long-term committed couples who pool all their money into joint bank accounts are happier in their relationship and less likely to break up than couples who keep some or all of their money separate . However, every couple knows what works best for them, so if you need to keep accounts separate or do a hybrid budget, more power to you!

Financial Planning for Millennial Couples

I've created a self-paced course for millennial couples to help them save and spend aligned with their values. We'll cover creating a tailored spending plan for you; we'll also talk about identifying values, understanding your money story, and collaborating on shared goals.

-

I cannot believe I am here today behind the mic recording the 100th episode of the Mind Money Balance podcast! I promise you we will get into spending plans versus budgets for couples but I need to start out by saying thank you. I want to say thank you to RJ Basilio, who has been here since day one editing this podcast. Liberty Sales joined me in June of 2021 and has done so much behind the scenes help on this podcast. And of course, I need to thank all of my amazing guests: Lauren Ranalli; Julie Tobi; Monica Kovach of Hold Space Creative; Alison Puryear of Abundance Practice Building; Leslie Togorda of New Moon Creative; Shari Loveday of Love WellTherapy; Jasmine Reed-Clark; Catalina Kaiyoorawongs; Danielle Wayne; Dr. Amy Nasamran of Atlas Psychology; Krista Carlin of the Curious Collective; Stephanie Gardner Wright; Taylor Broughton of Just Human; Stevon Lewis; Nathan Astle; Dr. Betsy Chung; Andrew Riesen of Heard; Dr. Kinga Mnich of the Ziva Way; Haneen Ahmed of Zane Counseling; Marissa Esquibel of Codpendummy; Danielle Bailey of Couch to Private Practice; Curt Widhalm and Katie Vernoy of Therapy Reimagined and the Modern Therapist Survival Guide; Raina LaGrand of Route to Rise Somatics; Dr. Devon Price, he wrote the book Laziness Does Not Exist and the new book, Unmasking Autism; Dr. Shainna Ali; Linzy Bonham of Money Skills for Therapists; Tiffany McClain of Lean in. MAKE BANK; Carryn Lund and Dr. Sharon Gold-Steinberg of Resourced Therapist; Dr. Alyssa Adams of the Uncommon Couch; Violeta Donawa; Joe Sanok of Practice of the Practice; Danielle Swimm of the Entrepreneurial Therapist; Dr. Marie Fang of Private Practice Skills; Josie Rosario; Annie Schuessler of Rebel Therapist; Allyssa Dziurlaj, Ed Coambs; Megan Costello; Sachiko Cohen; Rachel Moore; Alli Douglas Guerrero; John Sovek and Courtland McPherson; and of course, thank YOU--truly my amazing listeners for subscribing, reviewing and sharing my work. There have been so many times when I am just humbled and floored when I hear from you about how my words are resonating with you. And those moments really keep me going. I want to send you my deepest gratitude. There's a statistic out there that most podcasts end after seven episodes and so we'll see how long this one keeps going. But I'm so happy to be here sharing episode 100 with you all. Okay, thank you so much for listening. And let's get on to Budgeting and Spending Plans for couples the final episode in this month's theme: couples and money.

What is a budget? Let's just start right at the top. So a budget is a financial planning tool where you determine how much money you will spend or save each month. And in order to get there you first have to understand how much money you earn and then that helps you decide how much money is going out. The goal of a household budget is to make sure that you spend less than you earn. Spending less than you earn helps you to save money each month and prevents you from living paycheck to paycheck. And most budgets separate your expenses into three different categories or buckets or whatever you want to call them: needs, wants, and savings. Needs are things like food, shelter, and medication transportation; wants are things like dining out traveling, upgrading your phone before your new one has a shattered screen. Mine is nice and cracked right now; savings could be for short-term things like upgrading your car creating or bulking up an emergency fund. Remember I talked about booking up an emergency fund in Episode 99. Or savings could go towards additional things like investing money in retirement or investing more money in retirement. And oftentimes budgets are percentage-based. So if you kind of can picture a pie chart, it'll sound like you can spend 30% of your income on housing or I'm budgeting 25% of my income on food and dining out and budgeting tends to get a bad rap because of its restrictive nature and budgeting also tends to come with a lot of emotional heaviness. Like if a client of mine makes mistake with budgeting they tend to use words like Oh I'm bad at budgeting, I can't stick to it. In couples, this usually sounds like We've tried it, but it just doesn't work for us. And in my head budgeting requires a lot of rigid tracking and adhering to somebody else's financial guidelines. For example, if you Google, like, how much should I spend on housing, almost always, there's going to be this 30% rule that pops up. There's this rule that has been recycled again and again, that you should spend no more than 30% of your income on housing. Did you know where this rule came from, I did some digging for a different article that I'm working on. And I learned, you're always learning something new, no matter what industry you're in, I learned that this 30% rule has nothing to do with like the actual cost of living, or how much housing costs. It's based on a 1979 HUD bill. So that's Housing and Urban Development. That said, in order to qualify for public housing support, public housing rent can be no more than 30% of a renter’s income. So this 30% role where you're not supposed to spend more than 30% of your income on housing has nothing to do with how much housing actually cost. It comes from a 40-year-old bill that says, you know, the government won't support public housing, if it's more than 30% of a renter’s income. Isn't that interesting. And these are the types of rules that keep getting recycled and replayed. And kind of pedaled without any real regard as to why. So if you have been here a minute, you know that the B-word budget is not my preferred term. I prefer the term spending plan.

So let's like, just gently move into what the heck a spending plan is. I mean, honestly, it's like tomato-tomahto. A spending plan is honestly the same thing as a budget, but it just has a nicer ring to it. I'm a therapist, I know the power of words and reframes and what we think about money that can really impact our relationship with it. So for me, calling a budget, a spending plan just feels better. Let's get into like brass tacks, though a spending plan really does function in a very similar fashion to a budget, in that you set goals for how much money you can safely spend each month. But there's more wiggle room, you can't see me because this is a podcast, but I keep making like a figure-eight shape with my hand. And you could also kind of imagine waves, right? There's, there are different ways that you can do this, and different ways to make it feel better for you. So for some people, they set similar percentage base limitations on their spending plan. Other people kind of do a no budget budget where they pay themselves first, and then you spend whatever is left over. That's how I do it. And a spending plan versus a budget is really a powerful reframe. So when you're in a partnership, and you need help figuring out how to track your income and expenses and making sure that you're saving for goals and paying your future selves. Maybe just stop calling it a frickin budget. A lot of my clients, I can literally see on the screen, like their shoulders drop away from their ears, they will say things like, Ah, thank you, thank you for calling it a spending plan. And you can call it whatever the heck you want, right? This is just my preferred term. And a spending plan, in my opinion, gives you more flexibility, instead of saying something like, you know how budgets are very like needs versus wants based. Instead of saying something like massages are a want and not a need. You get to decide if there's money available in my account. And I have covered all of the things that I need to cover, then I can safely spend that money on a massage. I heard a Ramseyer. Those are. That's my term for people who follow Dave Ramsey. Say that allowing yourself to spend on one's "encourages overspending and not prioritizing future security" which is a little like it's really overemphasizing the need for hyper discipline and rigid rules and not breaking rules. And this idea that if you do anything out of alignment with these, like gridlocked pie charts, then you're bad. And I know as a therapist that rigid rules for most people are bound to backfire. That's why in all of my work, whether I'm working with couples or individuals, we always build in room for mistakes. It is not an if you make a mistake, it is a when you make a mistake, how will you cope, what will you do? And I know that it's so much better for us to give ourselves the ability to enjoy life, to enjoy our money, wow, we are saving for our future. It's not black or white. It's not all or nothing, it's both. And you can save for your future and enjoy something in the here and now. And when you have a spending plan, you can decide how much you are able to safely afford to spend on things in the here and now. And so a spending plan is important because it's the foundation of creating a healthy financial plan. Having a spending plan means you know how much money is coming in. And you have a flexible plan for how much money is going out every single month. And a spending plan that works for couples is something that helps them to make sure they're not living paycheck, paycheck to paycheck, and it builds in the room for future planning.

Instead of a budget that says you can only spend X dollars on things that fall into this category, a spending plan says you are allowed, you may spend up to x dollars on things. And if you spend more, it's no big deal, you just have to dial back your spending in a different area. So my partner and I have been doing a spending plan, no budget budget for ever. I honestly don't know how long we've been doing it. We broke all the rules of personal finance and bought a house together before we were engaged or married. So we have had a blended financial plan for a very long time. And so for us, our spending plan looks like auto-saving for things like student loans. So at the time of this recording, it's April 2022, and they are still on pause. But my partner and I are still putting money away each month to put towards those student loans. Now I know other people are like, you should be investing that money which may be true. But for our risk tolerance, we'd prefer just to have it available in cash so that when those student loans turn back on, we can pay off a solid chunk of them right away without having to pay interest on them. And you know, fingers crossed, the Biden administration does some sort of blanket student loan forgiveness, my crystal ball, I think we're probably going to get like a 10k Forgiveness kind of across the board. But do not quote me on that this is a hypothesis. This is not financial advice. But that's kind of what we're envisioning. So we save money automatically every single month to pay back student loans when so as turned on, we also automatically save money for vacations, gifts, and irregular expenses, or regular expenses are also called things like a sinking fund. So it's for those random things that happen that don't necessarily warrant dipping into an emergency fund. But it's nice to have a cushion for you know, random things like the faucet broke, and we need a new one. That would be something that wouldn't for us be considered an emergency because we have money set aside in an irregular expenses account. And again, you can Google it, some people call it a sinking fund. So after those savings buckets are funded automatically, then our spending buckets are filled up. And so for us that looks like a general spending bucket that kind of pays for all of the things that we can automatically so our mortgage or utilities, car insurance, things like that also gets like auto paid. And then we have a bucket of money for like the things that we don't rigidly adhere to, but we spend on every month so things like groceries, transportation, and pet care, those buckets kind of fluctuate for us, but we know kind of roughly what we'll be spending so we kind of set aside money for those things. And then we get fun money and fun money is my favorite thing ever. I recommend it to most couples. It is this idea that like whatever is left, you get to spend, and for my partner and I, we each get an amount that we are allowed to spend how however we want. So for us some recent spending plan purchases that were not divvied up into theirs and mine, but they were like a celebratory birthday brunch with friends a date night in streaming a movie and ordering takeout, and a last-minute visit with family, and then for our individual fun monies. In the olden days. I'm actually really curious what people call it I call pre-pandemic days, the olden days. Some of you call it like the before times, I will be so curious to hear what you refer to that era, the pre-March 2020 era but anyway, in the olden days, we would literally go to the ATM on the first of the month withdraw cash and each of us would have cash in hand that we could spend. However, we wanted no judgment from the other person. Nowadays, we do everything digitally. So we can have the same thing. We fill our digital envelopes or digital cash envelopes. That way we can kind of spend how we'd like. So again, I could save up for months and go treat myself to a day at the spa. Or I could spend it down to zero every single month, if that felt good to me, and there's no judgment for my partner and vice versa.

So a spending plan works for you like how do you know if it's actually working, it works for you. If you are spending less money than you earn each month, you have a system to track what's coming in and what's going out. And you're feeling good about not only where your money is going, but you're feeling good about your communication with your partner about your financial plan. So when it comes to spending plans for couples living together, having this financial plan isn't just important for managing like the finances of the household. To me, it's also about creating intimacy. Stay with me here. When you agree with your partner about your current and future financial goals, you are essentially saying, I want to be with you, I see a future for us together. I'm invested in this relationship, or to strengthen even more using we language we want to be together, we see a future for us together, we are invested in this partnership, in creating a spending plan and talking about money is really vulnerable. It's a great way to also see that you can do hard things you can collaborate on things that might feel a little bit awkward or uncomfortable and find a plan that works for you.

So there are kind of three common ways that couples can set up their spending plans together. So joint which is ours. When I say ours, I don't mean my partner, and I mean like ours bucket separate mine, and theirs, or hybrid. There's Mine and Ours. So with the joint account, everything, all money coming in goes into one account, all money going out goes out of one account, everything is shared, everything is commingled it is not. It's like once it goes in the pot, it's all together. Okay, separate is exactly what it sounds like you have a mine account and their's account, your money goes into your account, your partner's money goes into their account, and you spend out of those accounts as well. Sometimes people who have things completely separate will like Venmo money back and forth to each other. Some people split it up and say all pay for rent, if you pay for utilities, you have to kind of get creative there and still communicate even if you keep thinking separately about how you're going to pay for joint expenses. So separate is an option. And then hybrid. It's out there as Mine and Ours. So most money goes into a joint account, some money goes into you each of your individual accounts. And I think there are pros and cons to each of these approaches. I will just say that a 2021 paper from the University of London actually found that long-term committed couples who have joint accounts only. So just our's account, are happier in their relationships and less likely to break up compared to couples that keep some or all of their money separate. That said, You know what works best for you. If you need to keep your account separate or do a hybrid budget, please, by all means, feel free to do that. I also tend to recommend separate and hybrid accounts more frequently, when it is maybe cohabitating couples who have had previous marriages that ended in divorce. Sometimes that's really important to keep some separation there. I also tend to recommend separate or hybrid accounts for anybody who's experienced financial abuse, because there's a lot of trauma around joining those accounts after having experienced financial abuse. Other reasons you might want to do separate or hybrid accounts are if the partners have children from previous relationships, are caring for a person in their family with a disability, or caring for an aging adult. Those are different reasons why you might need to have separate or hybrid accounts. So take everything that I say through the lens of what works for us and do it cool.

So that's the why behind spending plans and budgets at the end of the day. They kind of function in the same way but I tend to find the reframe to a spending plan tends to work better for most people. And if you are a millennial couple and you're looking for some guidance on how How the heck can we figure out this spending plan things so we can spend and save in alignment with our values, I want to invite you into my live course Clarify Your Money: for Couples. Over the course of six weeks, not only will we cover how to create a tailored spending plan that works for you we'll also talk about identifying your values, understanding your money story and your partner's money story, and how to collaborate with your partner on shared goals. I created this course because my practice is full and bursting at the seams. And I decided at the end of last month that I'm no longer taking couples into my couples therapy practice or into Emotionally Focused financial coaching. Because to be honest with you, like the first four to six sessions, with almost every couple are really, really similar. And so I thought this would be a great way to take what I am doing in those sessions and bring it to you at a more economical price point. And it's the ability to kind of say, like, Look, I've been saying the same thing again and again, why don't folks who are in my audience who need help with this have access to it, I'm really excited to bring it to you. There is no shame here. There's no rigidity here. It is really about you and your partner saying look, we need some guidance here. And doing it and of course allows you to do it where I would love for you to show up live when possible. But if you can't attend live, that's no big deal. Everything will be recorded, and you can watch it on your own time. So you can kind of say, Look, this fits into our time we are this fits into our life. We are going to carve out the time for this. We've continued to put a spending plan on the backburner and we really want to work on some of those other nine goals that Lindsay laid out in Episode 99. But in order to do that, we need to have the spending plan figured out so if you are interested, please go to MindMoneyBalance.com/Clarify Again, that's MindMoneyBalance.com/Clarify To learn everything you need to know and to register. I will see you next week.

Transcribed by https://otter.ai